Just last week, a buddy of mine posed an intriguing question: “How long would it take to double my investment?” It’s a question that many investors ponder. Interestingly, I had recently come across a graphic on LinkedIn, shared by someone I follow, that discussed the timeframes for doubling investments across various assets. However, I was a tad sceptical about the data and its methodology, prompting me to delve deeper into the topic.

Doubling money is prevalent, but the approaches vary

Doubling your investment essentially means increasing its value to twice the initial amount. Achieving this, however, demands a blend of strategy and expertise.

Experienced traders, over time, have formulated various rules or techniques to gauge this duration, each based on specific assumptions and simplifications. Some prevalent methods include:

- The Rule of 72: By dividing 72 by the annual rate of return, you can estimate the number of years required to double your investment. While it’s a handy rule of thumb, it doesn’t factor in many variables influencing your investment’s growth.

- The Exact Formula: This method employs the natural logarithm function to determine the precise number of years to double your money. It offers a more realistic estimate but demands a bit of mathematical prowess and a calculator.

- The Rule of 70: Similar to the Rule of 72, this rule suggests dividing 70 by the annual rate of return for a slightly more accurate estimate, especially for lower returns.

- The Rule of 69: Here, you divide 69 by the annual rate of return and add 0.35. This rule is a tad more precise for higher returns and continuous compounding.

Other notable methods include the 114-rule, 144-rule, rule of 115, and the ever-popular compound interest. In this post, I’ll primarily focus on the Rule of 72 and compound interest to explore the journey of doubling your investment.

Using the rule of 72 to double your money

The Rule of 72 stands as a straightforward formula designed to gauge the number of years needed to double your investment at a specified annual rate of return or interest. Beyond just investments, it sheds light on the long-term implications of annual fees on an asset’s growth trajectory.

Interestingly, the Rule of 72 isn’t exclusive to investments; it’s applicable to any metric that grows exponentially, be it GDP or inflation.

To harness the Rule of 72, simply divide 72 by your investment’s annual rate of return. This will give you an estimate of the years it’ll take for your capital to double.

Let’s break it down with an example: if your investment yields a 6 percent return, it would take roughly 12 years for your money to double.

Formula: Rule of 72 (72) ÷ Annual rate of return (6) = 72 ÷ 6 = 12 years.

It’s worth noting that the Rule of 72 delivers its most precise estimates when applied to an 8 percent interest rate. As you deviate further from this 8 percent benchmark, either higher or lower, the accuracy of the rule diminishes.

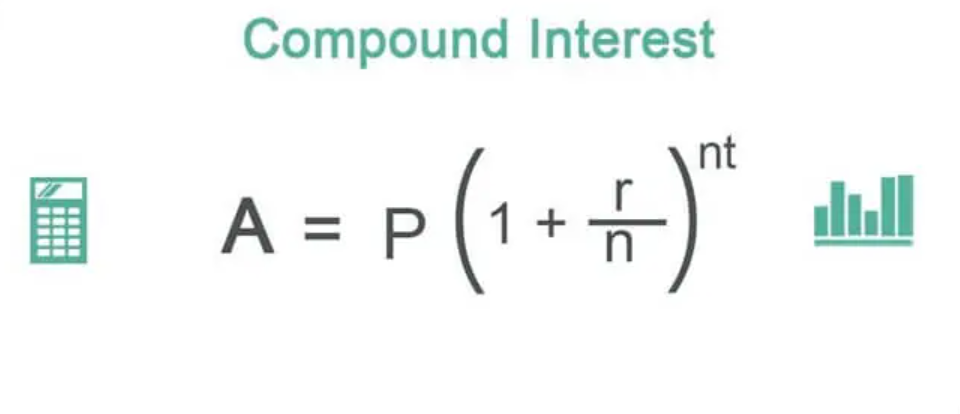

Using compound interest to double your money

The compound interest formula offers another lens through which we can determine the time it takes for our investments to double. This method employs the natural logarithm to provide a more accurate estimate of the time required for an investment to double, given a specific interest rate.

Here’s the compound interest formula for doubling money:

FV=PV×(1+r)n

Where:

- FV = Future Value

- PV = Present Value

- r = Interest Rate

- n = Number of Time Periods

Let’s assume an initial investment (PV) of $500. If we aim to double this amount, the future value (FV) would be $1,000. Plugging these values into our formula, we get:

1,000=500×(1+r)n

Dividing both sides by 500, we get:

2=(1+r)n

To remove the exponential expression, we’ll use the natural logarithm:

ln(2)=n×ln(1+r)

Simplifying further, the natural logarithm of ln(1+r) becomes r. Hence:

ln(2)=n×r

To determine the number of years, n:

n=ln(2)/r

Given that the natural logarithm of 2, ln(2), is approximately 0.693:

n=0.693/r

This equation allows us to determine the time it takes for an investment to double, given a specific interest rate. This is the foundation of the “Rule of 69.3,” which is derived from the rate.

Below is a table illustrating the number of years required to double an investment using both the Rule of 72 and the natural logarithm method, across interest rates ranging from 1% to 20%.

| Interest Rates | Rule of 72 # of Years | Log 63.9 # of Years | Differences in Years |

| 1% | 72 | 69.7 | 2.3 |

| 2% | 36 | 35.1 | 0.9 |

| 3% | 24 | 23.5 | 0.5 |

| 4% | 18 | 17.7 | 0.3 |

| 5% | 14.4 | 14.3 | 0.1 |

| 6% | 12 | 11.9 | 0.1 |

| 7% | 10.3 | 10.3 | 0 |

| 8% | 9 | 9.0 | 0 |

| 9% | 8 | 8.1 | 0.1 |

| 10% | 7.2 | 7.3 | 0.1 |

| 11% | 6.5 | 6.7 | 0.2 |

| 12% | 6 | 6.2 | 0.2 |

| 13% | 5.5 | 5.7 | 0.2 |

| 14% | 5.1 | 5.3 | 0.2 |

| 15% | 4.8 | 5.0 | 0.2 |

| 16% | 4.5 | 4.7 | 0.2 |

| 17% | 4.2 | 4.5 | 0.3 |

| 18% | 4 | 4.2 | 0.2 |

| 19% | 3.8 | 4.0 | 0.2 |

| 20% | 3.6 | 3.8 | 0.2 |

The interplay of interest rates and time

Interest rates and time share an inverse relationship. As the duration increases, interest rates tend to decrease, and the converse is true. Through the lens of the Rule of 72 and compound interest, it becomes evident that the time required to double an investment diminishes as interest rates escalate.

For instance, with an annual return rate of 20%, it would take approximately 3.6 to 3.8 years to double your investment.

Inflation and taxes: The double-edged sword

Inflation represents the rate at which the average price level of goods and services climbs, leading to a decline in the purchasing power of money. In simpler terms, as inflation rises, the same sum of money will fetch you fewer goods and services.

Let’s say the inflation rate stands at 2% annually. A bread loaf priced at $1 today would likely cost around $1.02 the following year. When you factor in inflation, the timeline to double an investment invariably extends.

Taxes, on the other hand, can substantially erode the actual worth of your investments. Various taxes, such as capital gains tax and income tax, can significantly diminish your investment returns, making the goal of doubling your money a more challenging feat.

For example, on a $2,000 investment with a 7% return ($140), if you’re liable to pay a 15% capital gains tax ($21), your net return dwindles to $119.

Tweaking the rule of 72 for inflation and taxes

To make the Rule of 72 and the compound interest formula more reflective of real-world scenarios, they can be adjusted to account for inflation and taxes:

For the Rule of 72:

Years to Double (Adjusted) = Annual Rate of Return−Inflation Rate−Tax Rate

72

For Compound Interest:

FV(Adjusted) = PV×[1+(r−Inflation Rate−Tax Rate)]n

Below is a table that contrasts the time required to double an investment using both the Rule of 72 and compound interest, while also considering the impacts of inflation and taxes.

| Interest Rates | Rule of 72 # of Years | Log 63.9 # of Years | Differences in Years |

| 2% | 51.5 | 49.9 | 1.6 |

| 3% | 34.3 | 33.4 | 0.9 |

| 4% | 25.7 | 25.2 | 0.5 |

| 5% | 20.4 | 20.2 | 0.2 |

| 6% | 17.2 | 16.9 | 0.3 |

| 7% | 14.7 | 14.5 | 0.2 |

| 8% | 12.9 | 12.8 | 0.1 |

| 9% | 11.4 | 11.4 | 0 |

| 10% | 10.3 | 10.3 | 0 |

| 11% | 9.4 | 9.4 | 0 |

Global Average Inflation Rate in 20221: 8.7%, Global Average Regional Tax Rate in 2022: 23.37%2

Contrasting nominal vs. real timeframes for doubling investments across interest rates

When we juxtapose the data from both the nominal and adjusted graphs, a striking observation emerges: the timeline to double an investment is significantly prolonged when we account for the influences of inflation and taxes.

Incorporating these real-world factors — inflation and taxes — into our calculations isn’t just a meticulous approach; it’s essential. They offer a truer depiction of how an investment will fare over time, ensuring that our expectations align more closely with reality. By doing so, we can make more informed decisions and set realistic financial goals.

Sources: International Monetary Funds1, Tax Foundation2

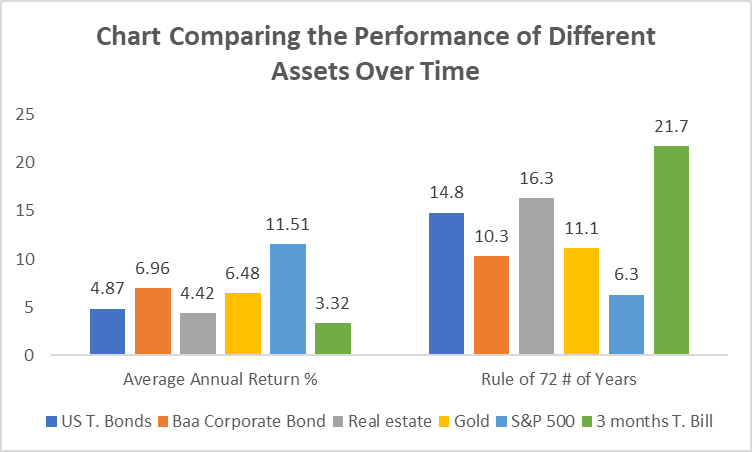

A glimpse into the historical efficacy of various investment avenues for doubling capital

Let’s delve into a succinct analysis of diverse asset classes and their historical performances spanning from 1928 to 2022:

| Asset Classes | Average Annual Return | Rule of 72 # of Years | End Value of $100 invested 1998/2022 |

| US T. Bonds | 4.87 | 14.8 | $7,006.75 |

| Baa Corporate Bond | 6.96 | 10.3 | $46,379.53 |

| Real estate | 4.42 | 16.3 | $5,121.52 |

| Gold | 6.48 | 11.1 | $8,866.76 |

| S&P 500 | 11.51 | 6.3 | $624,534.55 |

| 3 months T. Bill | 3.32 | 21.7 | $2,140.51 |

The S&P 500 includes dividends

From the data presented, the S&P 500 emerges as the most volatile investment option. Yet, its high-risk nature is counterbalanced by an impressive annual rate of return, clocking in at 11.51% between 1928 and 2022.

Applying the Rule of 72, an investment in the S&P 500 would approximately double in under 7 years, making it the swiftest among the lot. Over the 94-year period from 1928 to 2022, an investment in the S&P 500 would have doubled over 14 times.

To put this into perspective, a mere $100 invested in 1928 would have burgeoned to a staggering $624,534.55 by the close of 2022. However, potential investors should tread with caution, given the inherent volatility of this asset class.

On the other end of the spectrum, the 3-month T. Bills stand out as the most secure investment option. Boasting an average annual return of 3.21%, they present a stark contrast to the high-risk, high-reward nature of the S&P 500.

Utilising the Rule of 72, it becomes evident that it would take a little over 21 years for this investment to double. Over the 94-year span from 1928 to 2022, this investment would have seen a doubling only 4 times.

To illustrate, an initial investment of $100 in 1928 would have matured to $2,140.51 by the end of 2022.

This historical analysis underscores the importance of risk assessment and long-term planning when choosing investment avenues. While high returns are enticing, they often come hand-in-hand with increased volatility. Conversely, safer investments might offer slower growth but ensure more stability over time.

The pros and cons of each investment option

| Options | Pros | Cons |

| US T. Bonds | Risk: Low risk as they are backed by the U.S. government.Return: Moderate returns, higher than short-term investments like T. Bills.Liquidity: Fairly liquid, especially for shorter-term bonds.Diversification: Good for diversifying a portfolio and reducing overall risk. | Return: Lower returns compared to stocks or corporate bonds.Liquidity: Longer-term bonds may have less liquidity. |

| Baa Corporate Bond | Risk: Moderate risk, but higher than government bonds.Return: Higher returns than government bonds.Liquidity: Generally liquid.Diversification: Adds variety to a portfolio. | Risk: Higher risk compared to government bonds.Liquidity: May be less liquid in volatile markets. |

| Real estate | Risk: Moderate risk, but can be lower if well-diversified.Return: Potential for high returns through capital appreciation and rental income.Liquidity: Illiquid but can be sold.Diversification: Excellent for diversifying a portfolio. | Liquidity: Generally illiquid.Risk: Market-dependent and location-specific risks. |

| Gold | Risk: Low to moderate risk, often considered a safe haven.Return: Generally lower returns but stable.Liquidity: Highly liquid.Diversification: Good for diversification. | Return: Lower returns compared to stocks or real estate.Cost: Storage and insurance costs. |

| S&P 500 | Risk: Higher risk but historically high returns.Return: High potential returns.Liquidity: Highly liquid.Diversification: Represents a broad cross-section of the U.S. stock market. | Risk: Subject to market volatility.Return: Potential for loss. |

| 3 months T. Bill | Risk: Extremely low risk, backed by the U.S. government.Return: Low but stable returns.Liquidity: Highly liquid.Diversification: Good for short-term holdings. | Return: Very low returns.Diversification: Doesn’t add much variety to a long-term investment portfolio. |

Source: NYU Stern1

Investments poised to double money in the upcoming decade

Given their historical returns and recent performances, coupled with their growth potential, the following three companies stand out as promising investment avenues for the next decade:

#1. Novo Nordisk Inc.

Emerging from Denmark, Novo Nordisk has swiftly become a cornerstone of the nation’s economic ascent. This pharmaceutical behemoth now boasts a market capitalization that eclipses $400 billion, even outstripping Denmark’s annual GDP. In a recent accolade, Novo Nordisk was crowned Europe’s most valuable company.

This financial prowess stems from its escalating sales, especially in the domain of obesity care products like Wegovy and Ozempic. With an investment nearing $2.6 billion in state-of-the-art Danish production facilities, Novo Nordisk underscores its commitment to spearheading innovation in diabetes and chronic disease treatments for the foreseeable future.

#2. Netflix Inc.

Netflix stands tall as a premier entertainment service provider, boasting a staggering 233 million paid memberships spanning over 190 countries. Since its IPO in 2002, the company has charted an impressive trajectory. To put this in perspective, investors have reaped gains exceeding 30,000% since its public debut.

Netflix’s journey from a DVD rental service to a global streaming behemoth is a testament to its adaptability and vision. Its disruptive approach has already upended the traditional TV programming model, and it’s poised to challenge the cable industry next. With a relentless focus on expanding its global footprint, Netflix is well-equipped to amplify its subscriber base.

#3. Tesla Inc.

Tesla, the vanguard of the electric vehicle (EV) revolution, has consistently dazzled the stock market over the past decade. The company’s recent financial disclosures highlight a record revenue nearing $25 billion, complemented by a substantial uptick in earnings. With the EV market forecasted to surge to a mammoth $212 billion in annual revenue by 2030, Tesla is strategically positioned to capitalize on this wave.

As a high-growth stock, market pundits believe Tesla could touch a valuation of $1 trillion in the upcoming decade, if not earlier. While the stock commands a premium, it’s widely regarded as a lucrative bet for investors with a long-term horizon.

Sources: Nasdaq1, CNBC2, Netflix3, Bezinga4, The Motley Fool5,

Conclusion

The aspiration to double one’s money is a common financial goal, and it’s more attainable than many might believe. Concepts like the Rule of 72 and compound interest serve as foundational tools to project the time frame needed to double an investment.

Yet, it’s essential to remember that real-world elements, such as inflation and taxes, can modify this timeline. By comprehending the risk and return profiles of various asset classes, investors can make more enlightened decisions.

FAQs

The Rule of 72 is a handy formula designed to approximate the years needed to double your money at a specific annual rate of return. Simply divide 72 by the anticipated annual return to get an estimate. It’s a swift method to assess the potential of diverse investment avenues.

Compounding is the mechanism where you earn interest not just on the principal amount but also on the accumulated interest. By consistently reinvesting your returns, your investment grows at an accelerated rate. For instance, with a 10% average annual return, your investment can potentially double in about seven years.

Both inflation and taxes can significantly impact the real returns on your investment. While inflation diminishes your money’s purchasing power over time, taxes can substantially reduce your investment gains. To factor in these elements, you can modify the Rule of 72 as: Years to Double (Adjusted) = 72 ÷ (Annual Rate of Return – Inflation Rate – Tax Rate).

While the Rule of 72 offers a convenient way to get a ballpark figure of investment growth, it’s not as accurate as compound interest calculations. Compound interest considers the periodic compounding of interest, delivering a more detailed projection of investment growth.

To harness the full potential of compounding and the Rule of 72:

Start investing as early as possible.

Ensure regular contributions to your investment.

Always reinvest your earnings.

Choose investment avenues that strike a balance between promising returns and manageable risks.