Analysis of Chinese investing strategy in China, and its implications for a possible buyout of PREM.

I have covered Premier African Minerals (LON: PREM) more times than I can count, across a half-dozen publishers since mid-2019. Until recently, I have been looking solely at PREM’s progress and milestones, which have certainly been impressive.

It’s worth noting that the company has gone from undeveloped bush to pilot plant in the space of a year — by industry standards this is practically unheard of.

And to be clear, there are many more RNSs to potentially report on through 2023, though these do seem more like exercises in tick-boxing as production brings the rewards closer.

These include, but are not limited to, confirmation that the ‘pilot’ plant has commenced production, the first sale from Zulu, the first receipt from Zulu, further assay results, output increases, news on a second plant, pilot plant optimization, solar energy plans, approval of its mining licence application for the wider EPO…

Further catalysts are pretty much endless. Unlike other favourites such as #HARL, #AVCT, or #BOIL, production is set to begin shortly, so there is a huge amount of information to convey to shareholders in the near term.

The other three have now confirmed their potential, so in those cases, regardless of share price movement, it’s simply a case of sitting tight and waiting out the dips, no matter how hard that may be.

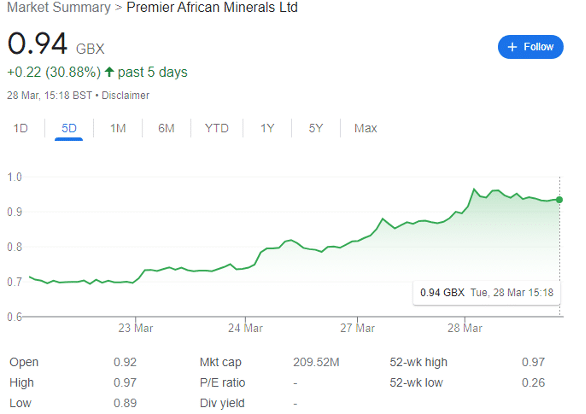

PREM shares are now riding high at 0.94p, having risen by a third in the past few days alone. The lithium explorer — soon to be producer — now has a market cap of over £200 million. And while profit-taking and the usual AIM nervousness means volatility may be inbound, further rises may be coming down the pipeline.

But why is this?

Yes, some of the recent spike can be attributed to expectations of profits from sales from Zulu. A maiden dividend may also be coming, though I would prefer all profits to be diverted to further development of Zulu or even to PREM’s other high-quality but often over-looked assets.

And arguably, there is an element of ramping. Despite being delighted with the recent spike, it’s also attracted the usual flies, who will quickly move onto the next AIM mover at the next available chance.

But the key underappreciated factor is that institutional investors — and indeed many retail investors — steer clear of explorers. I have lost count of the number of promising explorers who have gone nowhere, and many institutions ignore them altogether, much in the same way as a recruiter might ignore a candidate without a degree for some roles, even if they have exceptional experience.

But PREM is — or soon will be — a producer. This puts it in a different category.

My view is that strategic investor and offtake partner Canmax Technologies (formerly Suzhou) could choose to either buyout the entire company, or offer significant additional funding in exchange for more shares, or pay a premium for the rights to 100% of production rather than the 50% at present.

It’s hard to know which of these avenues could be more appealing. Canmax Chair and multi-billionaire Pei Zenzhue — who also owns a 5.8% stake in CATL — visited the site in early January and left with a strongly positive view. And Zenzhue already has multiple other investments in Zimbabwe.

But some clues for his potential approach can be found in the changes to Chinese investment strategy into Africa — with priority in the past given to security of supply over attempting to gain overall control.

Chinese investing strategy

Understanding whether PREM could be subject to a buyout requires a long-term professional view of Chinese mining industry interests in Africa. And Africa accounted for 12.3% of Chinese companies’ exploration and strategic investment budgets in 2021, up from 8.1% in 2011.

Partially, this is due to the CCP wanting to reduce dependence on Australia should they choose to invade Taiwan. But it’s also worth noting that Australia is far more expensive to invest in, with the former trade-off being increased confidence in Australia’s regulatory and judicial systems.

For example, mine costs at Chinese titan CITIC’s iron ore mine in Australia have been high since operations began, with all-in sustaining costs over $100/dmt in 2013 and 2014 alone. These costs have only risen with time, as the ore requires a four stage milling process compared to the usual standard of two, while labour costs are also high by international standards.

Importantly, high operating costs came from a lack of preliminary study of the project — and this rush to achieve dominance in the project came under harsh criticism from domestic Chinese investors and the Communist Party itself, who were less than impressed with the message of incompetence sent to the global markets.

Since this mistake, Chinese companies have been encouraged to take a different strategy.

Take copper. Of the 88 Chinese-owned copper assets abroad, 17 are owned by China Nonferrous Mining Corp — and all 17 are in the Central African Copper Belt.

One of the earliest mines it acquired was the Chambishi Project in Zambia — bought in 1998 — and the project was also subject to limited due diligence. Now it’s one of the highest-cost copper mines in the world. The Chinese learnt from their mistakes, instead preferring to become strategic investors in smaller mines such as Zambia’s Muliashi North in 2009, which is now one of the lowest-cost copper mines.

This approach — sometimes involving selling off higher-producing-cost stakes — leaves S&P Global data showing that African-sourced copper destined for China is now the lowest cost of all copper-producing regions. And the strategy that has worked is clear — making a strategic investment in return for security of supply and with the understanding that divestment could occur if feasibility studies come back with high-cost results.

But Africa is also becoming more attractive because to a large extent it’s cleared up its act with regards to regulation.

For example, when Blue Orca launched its short attack on Atlantic Lithium’s Ghanian operations, the accusations of bribery didn’t hold the same water as they may have in the past. And Vast Resources has been awarded those contested diamonds by the Zimbabwe High Court — partially as the country wants to project an image of investibility and judicial fairness.

Of course, Africa is a massive continent comprising 54 recognised countries, so this is something of a generalisation. But the trajectory of increased judicial confidence means that it is far more investible than in the past.

Now to specifics.

Chinese investment into African mining has been predominantly funded by state-owned enterprise, but private companies have also been hugely encouraged by Beijing’s 2014 simplified approval procedure for foreign investments in mining exploration — regulated by the China National Development and Reform Commission — for projects valued below $1 billion.

This little-known law — part of the Belt and Road Initiative — effectively highly encourages private companies to make small investments in dozens of African-based explorers — whether in iron, copper, lithium, or others — to reduce risk of failures and also prioritise security of supply. In the case of PREM, it’s worth noting that our offtake partner has rights to 50% of the lithium but only owns less than 13.38% of the company.

Now let’s look at a key case study.

Zijin Mining Group has the most foreign mining assets of any Chinese company — 47 at present (though I cannot verify this figure independently). It has completed eight deals in the past two years, and 21 acquisitions or strategic investments since 2010. The majority of these acquisitions has been in the gold sector, and overseas gold production is expected to constitute 52.7% of the company’s gold production by 2028.

But the key information is that Zijin initially prioritises security of supply by providing funding for pilot plants in exchange for some shares, and then seeks outright control once production is proven to be low-cost and economically feasible.

One advantage that Chinese companies — and state-owned enterprises — have is that they are less beholden to shareholders, and therefore can ignore the boom-and-bust mining supercycle when making investment decisions.

Indeed, western-listed miners are actually decreasing investment in maiden resources as the world goes into recession, as investors fret over the short-term depressive effect on commodity prices, even though the longer-term supply gap means prices are only heading one way over the longer term.

But Chinese companies play the long game. They know that supply is what matters most, as the lithium price will rise when the gap widens over the next decade. Arguably, CATL’s battery pricing strategy is designed to bring the lithium price down artificially — leaving a certain major shareholder able to buy shares in lithium companies cheaper than would otherwise be possible.

The Kodal Minerals deal has shown, unequivocally, that China is desperate to secure supply. The conditions of the deal are extremely favourable to the company — and PREM could be next to dictate terms.

China and Zimbabwean Lithium

Lithium reserves have been found all over Zimbabwe, Namibia, Ghana, the Democratic Republic of the Congo, and Mali. But while I could write a few dozen pages on how Chinese strategy works elsewhere in Africa, PREM is located in Zimbabwe, so I will focus here.

The country has been mining lithium since the 1960s, and the government thinks that thee Chinese-owned Bikita mine 300km south of the capital has circa 11 million metric tons of lithium resource. The World Trade Organisation considers that Zimbabwe will one day meet 20% of peak global lithium demand, and it is already the world’s sixth -largest producer of the silvery-alkali metal.

Of course, much has been made of December’s Base Mineral Export Control Act, which bans the export of raw lithium. Aimed at so-called ‘artisanal’ miners (which supports the livelihood of 1 million Zimbabweans), the government estimates it has already lost $2 billion in minerals smuggled across the border by artisanal mining leakage.

But the law is also aimed at getting companies to invest in Zimbabwean plant building and processing capacity, and therefore is no bad law by any means. The country should benefit from its natural resources — and Roach has made clear that this is a priority. Further, many artisanal miners are horrendously exploited, and while some may lose their means of work, others will be freed from what is effectively slave labour.

One key part of the law is that companies already in the process of developing mines — including giants like Zhejiang Huayou Cobalt, Sinomine Resource Group and Chengxin Lithium Group (which have collectively invested $678 million into lithium projects in the country) are exempt.

And last year alone, Chinese titans including Tsingshan, China Nonferrous, and Huayou Cobalt invested nearly $1.5 billion in Zimbabwe. Meanwhile, Sinomine Resource Group has announced its plans to expand production at Bikita mine by investing $200 million into building a new lithium plant.

But who else is excluded from this new law? Premier African Minerals. This makes the company one of the last potential full acquisitions that China can make into Zimbabwean lithium without being constrained by the law — both Zimbabwean law limiting the export of unrefined lithium, and Chinese law making it incredibly difficult to invest more than $1 billion in any one acquisition.

Consider this: Sinomine acquired Bikita for $180 million in 2022 and has created a JV with Chengxin Lithium Group’s Zimbabwe unit to increase lithium projects in the country. And Chengxin itself paid $76.5 million for 51% of the Star Lithium mine blocks in 2021. Zhejiang Huayou Cobalt, meanwhile, bought the Arcadia lithium project for $422 million deal in 2021 — and plans to invest a further $300 million into a processing plant at the site.

These huge investments into new lithium processing plants are leaving massive extra processing capacity. And the EPO of Zulu is huge.

This is why — in my view — the buyout is coming and coming fast.

Production is starting, so Chinese historical nervousness of investing too heavily in exploratory companies is no longer as relevant. China is already building huge amounts of infrastructure, which will significantly reduce capex costs. PREM is also not covered by restrictive new laws, so any buyer can ship out unrefined lithium — a privilege that will not be afforded to any future explorers.

And with a £208 million market cap, a buyout price of 3p — or circa £600 million — leaves PREM comfortably below the $1 billion maximum investment allowed under Chinese law.

But if PREM gets to 3p before an offer is made, then the Chinese will miss the buyout boat.

QED.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

Excellent thoroughly researched and a timely article