High-risk, high reward. Exploratory mining, 129,400 carats of diamonds, and an explosive share price. My cup of tea.

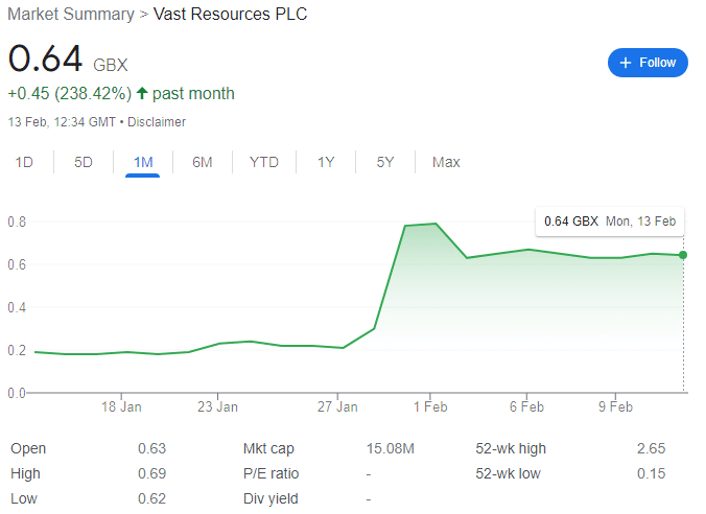

Vast Resources (LON: VAST) shares rocketed from 0.21p on 27 January to 0.79p by the start of February as the FTSE AIM miner announced exceptionally good news — more on that later — to investors.

However, the stock has retraced back to 0.64p over the past fortnight and remains down 56% over the past year — a year of significant chart volatility. For potential investors, the question is this: is the share price dip from the recent high an opportunity, or have we missed the boat?

Vast Resources: interests in brief

VAST is a £14 million London-listed exploratory miner with assets in projects across Romania, Tajikistan, and Zimbabwe.

In Romania, VAST is focusing on rapidly advancing high-quality projects by recommencing production at previously producing mines. Its portfolio includes a 100% interest in Vast Baita Plai SA which owns 100% of the already-producing Baita Plai Polymetallic Mine, located in the Apuseni Mountains, an area which hosts Romania’s largest polymetallic mines.

Baita Plai has a JORC compliant Reserve & Resource Report which underpins the initial mine production life of approximately 3-4 years with an in-situ total mineral resource of 15,695 tonnes copper equivalent, with a further 1.8-3 million tonnes exploration target. VAST is now actively working on confirming an enlarged exploration target of up to 5.8 million tonnes.

VAST also owns the Manaila Polymetallic Mine in Romania, which it’s looking to bring back into production following a ‘period of care and maintenance.’ The FTSE AIM company has also been granted an Extended Exploitation Licence to re-examine the exploitation of further mineral resources within the larger Manaila Carlibaba licence area.

Vast also has an interest in a revenue JV from the 100% financed Takob Mine processing facility in Tajikistan. This will provide Vast with a 12.25% royalty equivalent over sales of non-ferrous concentrate and any other metals produced.

And in Zimbabwe, VAST is finalising a JV mining agreement on the Community Diamond Concession, Chiadzwa, in the Marange Diamond Fields.

Financial details

In recent interim results, VAST saw revenues in the six-month period to 31 October increase by 69% to $1.93 million. Meanwhile, losses after taxation in the period decreased to $6.78 million, down from $7.32 million in the year-ago half.

Cash at the end of the period was at circa $600,000, and the company’s debt stood at $8.9 million. These kinds of losses aren’t unusual in exploratory mining, but with the cash runway almost out, on 6 February the inevitable occurred, and Vast issued a placing of circa 433.2 million new shares to raise £2,382,500 at a share price of 0.55p.

The cash will be used to continue the ongoing drilling and production ramp up at Baita Plai to achieve name plate capacity of 14,000 tonnes per month — and VAST claims that ‘production at Baita Plai continues to exceed projections and the Company is on track, based on current commodity prices, to achieve name plate capacity in H1 2023.’

Importantly, CEO Andrew Prelea participated in the placing, acquiring 15 million shares for £82,500 of his own money. Skin in the game is a key indicator that management truly believes in their company — and is as close as outside investors can get to quality insider information as possible while staying on the right side of the law. Management do not buy shares in a doomed cause.

VAST diamonds

On 2 February, VAST announced that the High Court of Zimbabwe had granted a default order against the country’s Minister of Mines & Mining Development over a long-running dispute — concerning historic claims to a parcel of 129,400 carats of rough diamonds held in custody at the Reserve Bank of Zimbabwe.

Hours after the placing on 6 February, VAST announced it had acquired the signed and stamped High Court Order. The company is in the process of initiating a ‘a lawful and transparent process for the release of the Historic Parcel into the Company’s possession.’

At this point, it’s probably not worth getting into the legal details of ownership of these diamonds; however, for brevity it seems that VAST has always had a — forgive the pun — rock solid claim. Many investors were rightly concerned that Zimbabwe’s High Court would nevertheless find against the company, and this ruling should be seen not just as a win for VAST, but also as a win for integrity of the country’s judicial system.

Cynically, it’s also in the government’s interest to demonstrate that Zimbabwe is a serious place to invest, and that there will be no rug-pull, either in terms of the law or good government for long-term investors. With mining, it’s often a decade from acquiring an asset to production, and stability remains the golden ticket to further external investment. Considering the Chinese investment into the country’s mining sector — look at PREM et al — the decision was almost certainly influenced by external factors.

Or in short, Zimbabwe is prepared to keep its legal word for further investment, including in VAST’s project in the Marange Diamond Fields. As Prelea notes, the order ‘demonstrates the Zimbabwe Government’s and in particular His Excellency President Cmd. E D Mnangagwa’s commitment to resolving legacy issues related to investment in Zimbabwe in a transparent and legal manner for the mutual benefit of investors.’

Valuation

The reality with VAST — and I am happy to hear the opinions of others — is that the company’s operations are, while not worthless, now irrelevant to its share price movement. This is not to say that the operations don’t hold promise, which of course they do. But before the diamonds came into play, it held a market cap of circa £5 million, and it’s now around £15 million.

These diamonds need to be handed over, if they haven’t been already. They need to be cleaned, valued, prepared, and then sold. And diamonds have disappeared without a trace from the central bank’s vaults in the past — including 350,000 carats worth an estimated $140 million in July 2021.

Importantly, VAST are unlikely to notify investors that they have the diamonds in their possession before they are sold, as I consider it likely that the company will arrange a sale to have the diamonds sold on directly from the vault at the Reserve Bank rather than take physical possession.

And here’s the rub — unless I’m mistaken, investors have no idea what these diamonds are worth. For perspective, one historical article suggests that the entire central bank stockpile including VAST’s diamonds is worth between $32 million and $1.7 billion.

Previous auctions of Zimbabwean diamonds have fetched an average of about $400 per carat, but this rises to $12,000 per carat for exceptional items. As a low ballpark, consider that VAST’s diamonds are below average, and sell for $300 per carat. At 129,400 carats, that’s $38.82 million. Excluding expenses, investors are looking at a rough profit of $35 million — more than double the current market cap.

And this excludes the value of its multiple exploratory operations. Of course, there’s also a possibility that the diamonds fetch the average of $400 a carat, or even far more.

This presents an interesting dilemma for the would-be investor. Assuming the diamonds are taken into possession and sold in a timely fashion, then the income should see the market cap at least double based purely on what would then be cash at hand. Indeed, it could go further than double, as VAST would then be well-capitalised to develop every asset it has at pace.

However, it can take weeks for a sale and transfer of diamonds to be agreed, and as I previously stated, I don’t think investors will get an RNS until this happens. This means the share price could drift slowly downwards as traders exit, leaving a better buying opportunity for long-term investors.

But wait too long, and the next explosive movement upwards will come when the diamonds are sold and the cash is in the bank. And this is still not risk-free. Until the cash is in the bank things can always go wrong.

But as a high-risk investor, a speculative investment is too tempting for me to ignore.

This article has been prepared for information purposes only by Charles Archer. It does not constitute advice, and no party accepts any liability for either accuracy or for investing decisions made using the information provided.

Further, it is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.